Executive summary

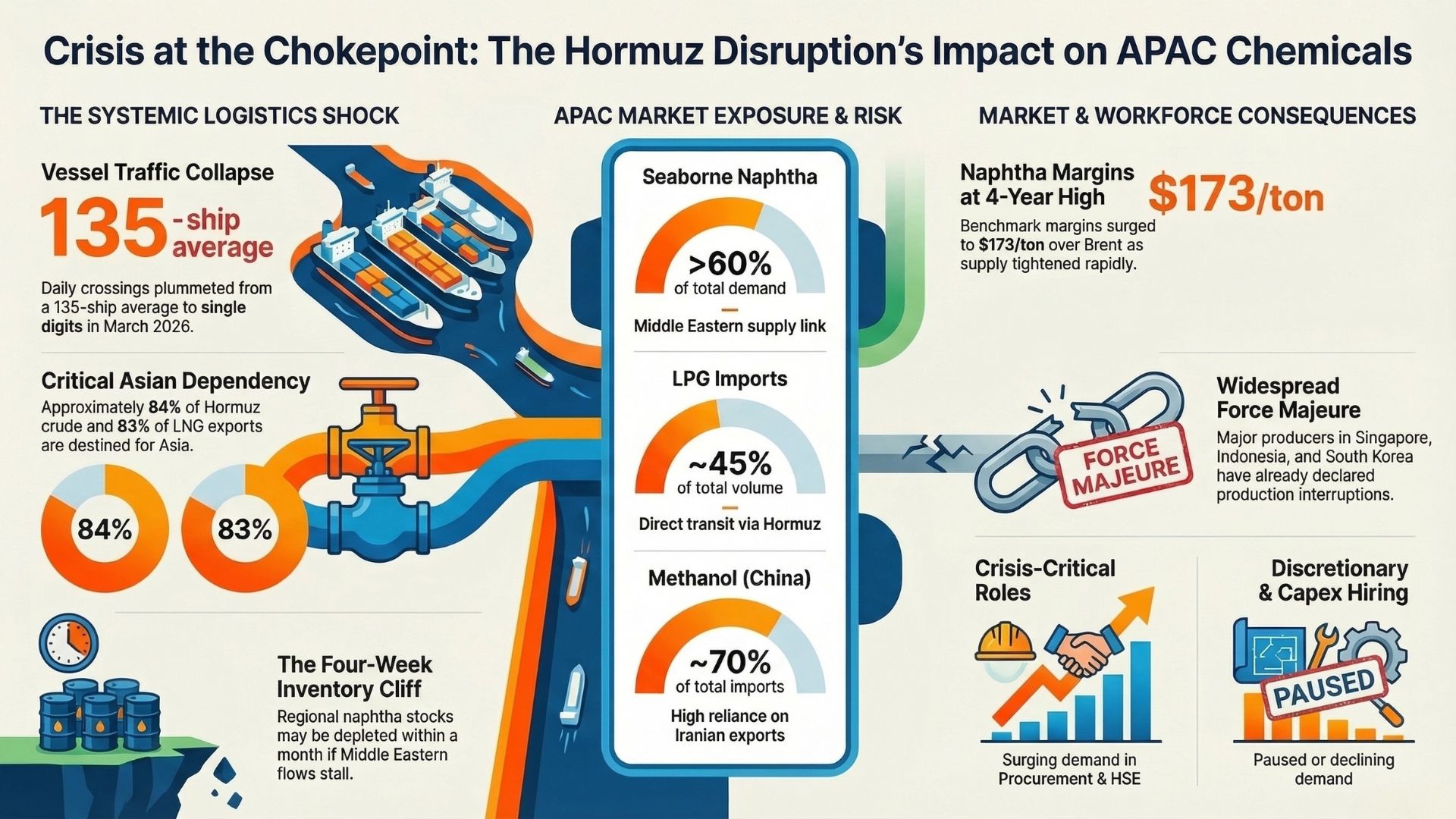

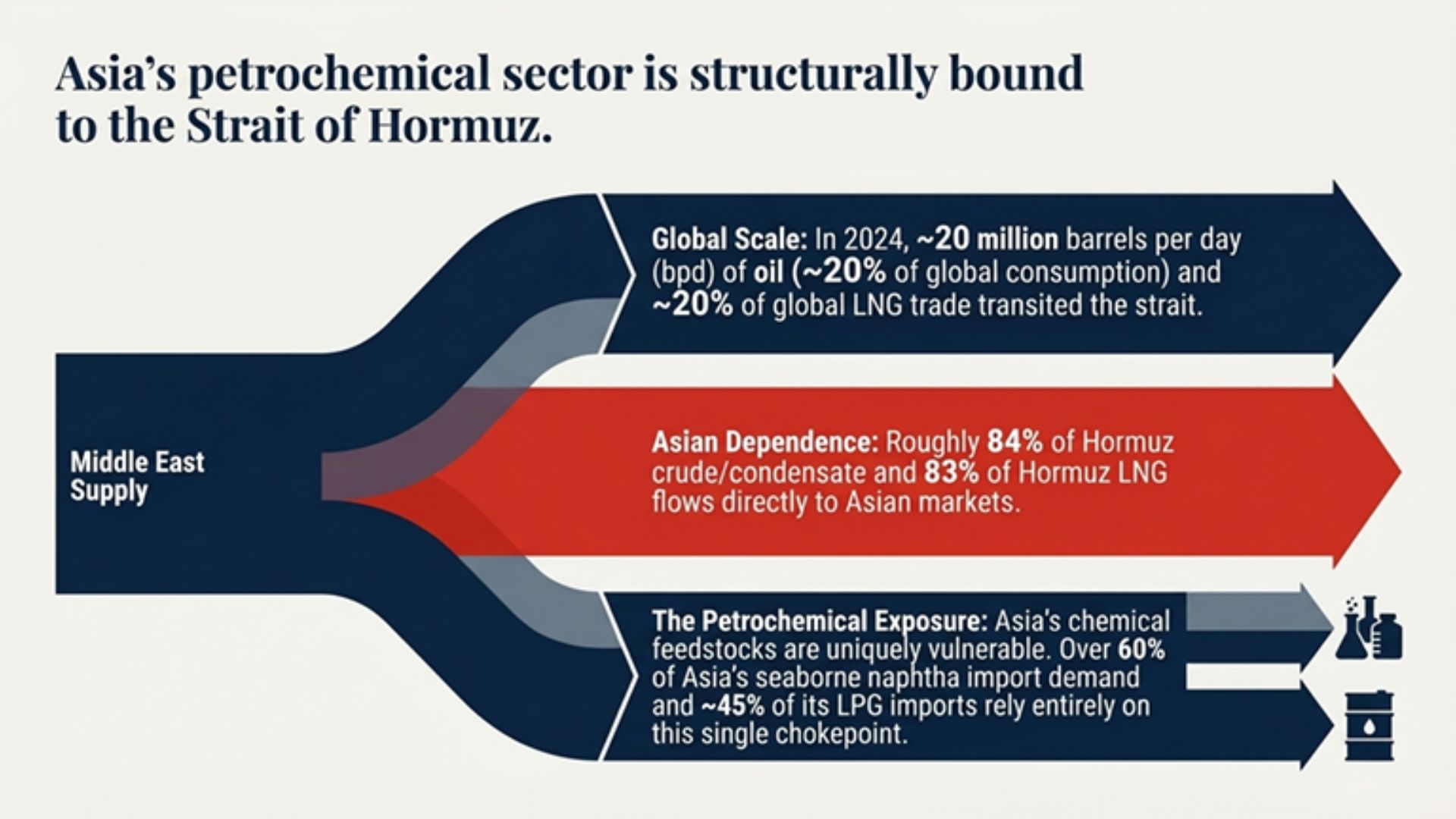

- The Strait of Hormuz is structurally “systemic” to Asia’s energy and petrochemical cost base: in 2024, oil flows through the strait averaged about 20 million barrels/day (~20% of global petroleum liquids consumption), and ~20% of global LNG trade transited Hormuz; ~84% of Hormuz crude/condensate and ~83% of Hormuz LNG went to Asian markets (with China, India, Japan, and South Korea the top destinations).

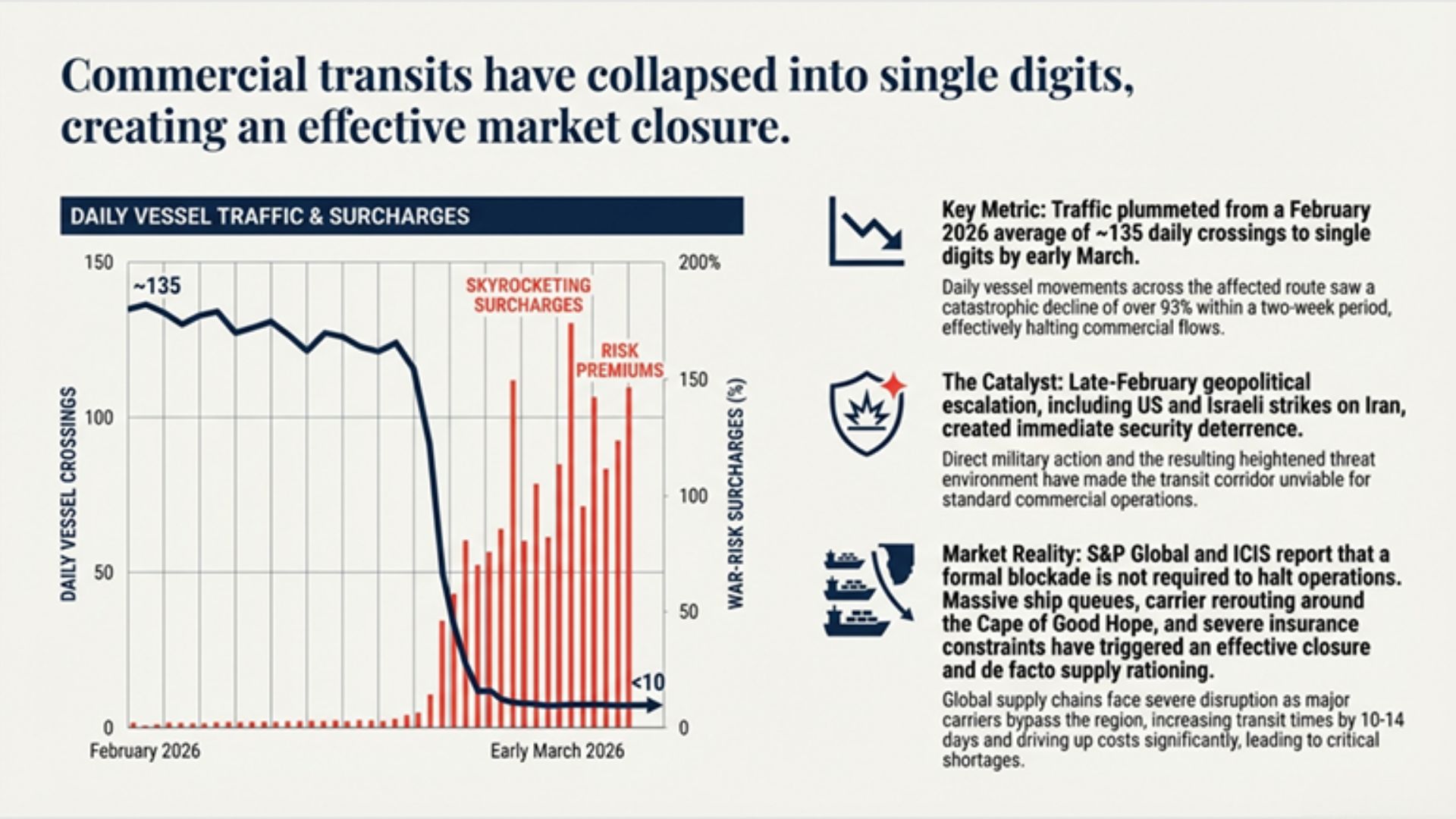

- In the current March 2026 crisis, shipping disruption is not theoretical: vessel traffic has collapsed from typical levels to “single-digit” daily crossings and a large queue of ships has formed, implying immediate schedule slippage, higher war-risk costs, and “de facto” supply rationing even where the strait is not formally closed.

- Asia’s petrochemical feedstock exposure is acute because the region is still largely crude/naphtha-linked: >60% of Asia’s seaborne naphtha import demand in 2025 was covered by Middle Eastern supply and ~45% of Asia’s LPG imports move via Hormuz; ICIS also cites that naphtha could be depleted in “about four weeks or less” if Middle Eastern flows remain stuck.

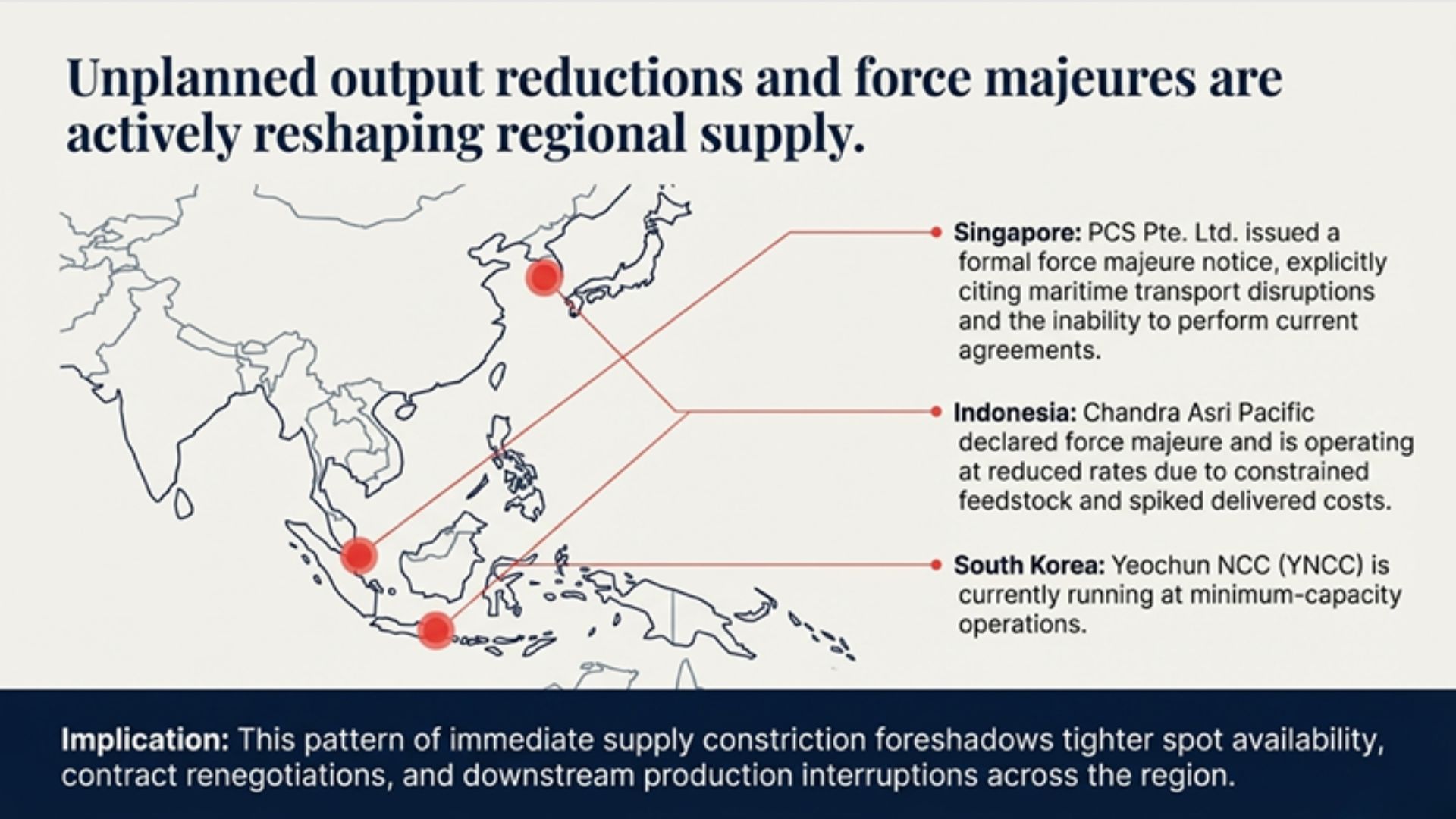

- Early operational evidence is already visible in SEA/APAC: force majeure declarations and output reductions have been reported/confirmed for multiple regional producers, including PCS (Singapore), Chandra Asri (Indonesia) and Yeochun NCC (South Korea)—a pattern that typically foreshadows tighter spot availability, contract renegotiations, and downstream production interruptions.

- Pricing and margins are moving quickly: Reuters reports Asia’s benchmark naphtha refining margin at a ~4-year high (~$173/ton over Brent), while ICIS describes PP market dislocation including halted offers, rerouting, and sizable war-risk premia; investor-side commentary in India is already modeling 10–20% interim price increases across parts of the chemical chain under constrained inventories.

- Hiring impacts across SEA/APAC are likely to be asymmetric: near-term, demand rises for crisis-critical roles (feedstock procurement, trading, logistics, price-risk, planning, HSE/process safety), while discretionary hiring and some capex-linked roles face delays—especially because much of APAC petrochemicals entered 2026 already burdened by overcapacity, restructuring pressure, and cash-preservation behaviors.

Situation update

The “present situation” around Hormuz (as of March 6, 2026, Asia/Kolkata) is best understood as a logistics-and-risk shock layered onto an already-fragile APAC petrochemical margin cycle.

- The proximate trigger widely cited in market reporting is a late-February escalation involving strikes on Iran by the United States and Israel, followed by attacks and elevated security risks that deter commercial transits.

- Independent energy analysis from U.S. Energy Information Administration explains why even “temporary” disruption matters: there are “very few” alternatives to move Gulf volumes if the strait becomes unusable, and pipeline bypass capacity is limited relative to normal seaborne flows.

- Market tracking and shipping intelligence (including entity [“company”, “S&P Global”, “financial intelligence firm”] and Reuters analysis) shows the disruption is operationally real: traffic fell from a February average of ~135 daily crossings to single digits on specific March days, and queues of vessels formed on both sides of the waterway.

Major container and liner operators have publicly adjusted routes and imposed surcharges, reflecting both physical risk and insurance constraints; Reuters cites rerouting around Cape of Good Hope and war-risk surcharges by carriers.

A key nuance for decision-makers: it may not require a formal “closure” for the chemical market to behave as if it is closed. ICIS characterizes the situation as an “effective closure,” and entity [“company”, “S&P Global”, “financial intelligence firm”] reporting similarly indicates “near-standstill” flows driven by security threats and shipowner risk reassessment.

Finally, Oman sits on one side of Hormuz in the standard geographic description used by EIA (the strait lies between Oman and Iran), which matters because the disruption is not only geopolitical; it is also a hard constraint on physical routing capacity.

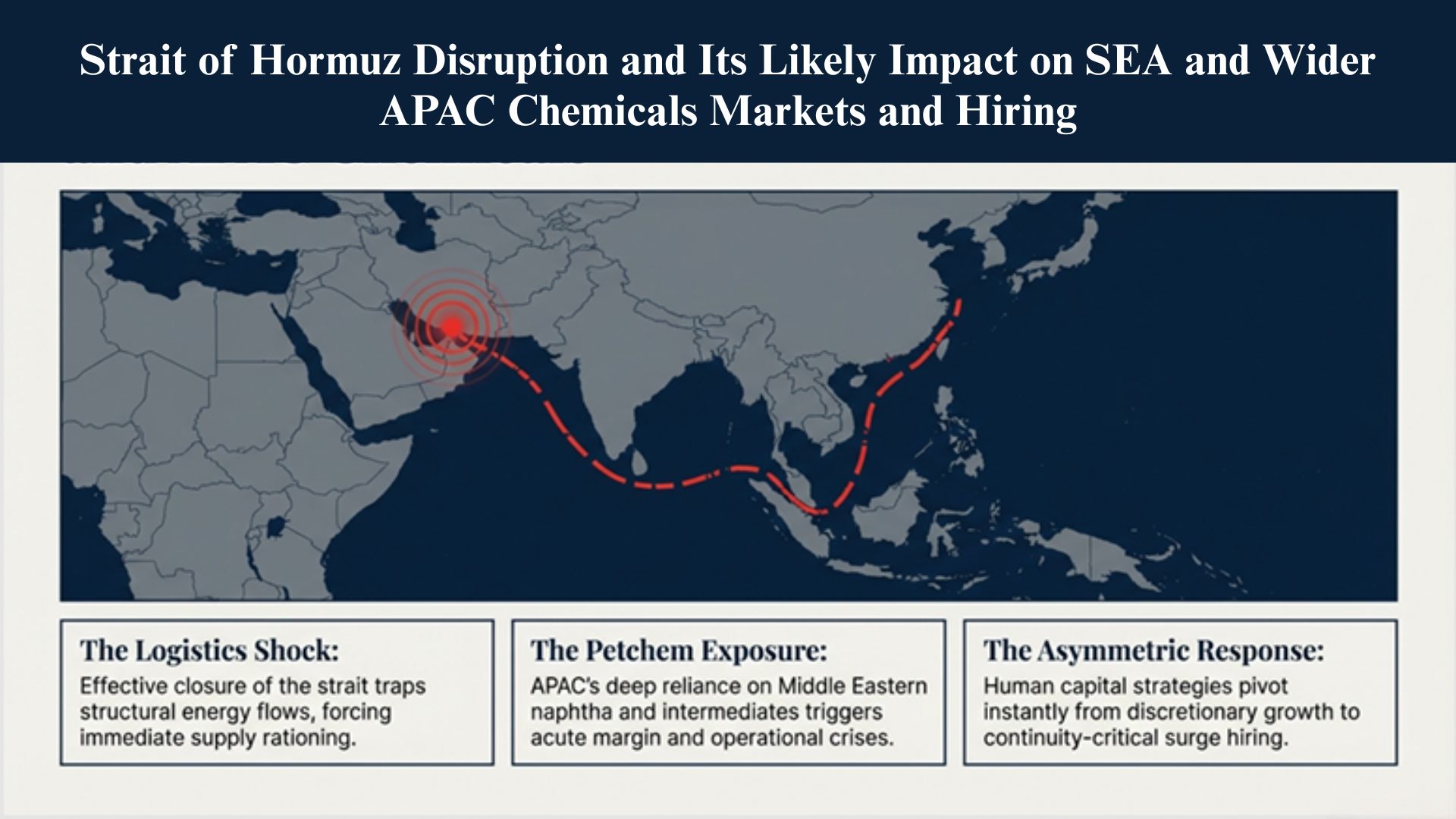

Exposure map for SEA and wider APAC

The “impact pathway” into chemicals is not one single channel: it’s a bundle of linked exposures:

- Hydrocarbon feedstocks (crude, naphtha, LPG, condensate) that drive marginal cost for olefins, aromatics, and refinery-petrochem integration.

- Chemical intermediates exported from the Gulf/Iran (methanol, MEG, fertilizers, polymers) that sit upstream of packaging, textiles, construction, autos, and electronics.

- Freight/insurance and route instability that changes landed cost and lead times even for non-Gulf origin cargoes (rerouting, conflict surcharges).

SEA and APAC: where the dependence is most immediate

- Singapore: the earliest “signal” is contractual and operational—PCS Pte. Ltd. issued a formal force majeure notice, explicitly citing disruptions to global maritime transport and broader supply chains, and stating it is temporarily prevented from performing obligations under current agreements.

- Indonesia: Chandra Asri Pacific has been cited in both Reuters and ICIS reporting as declaring force majeure and running at reduced rates, consistent with constrained feedstock inflow and higher delivered costs.

- South Korea: Reuters reports the country sources 54% of its Middle East naphtha supply via Hormuz, and early decisions are time-compressed—buyers may have to decide “within the next two weeks” whether to seek alternative regions or cut output; ICIS and Reuters also reference South Korean producer force majeure and minimum-capacity operations.

- Japan: Reuters reports cancellations of April naphtha import tenders by Japanese buyers amid uncertainty; ICIS also notes potential cancellations of March/April arrivals and the risk of reduced refinery runs that further tighten aromatics co-products.

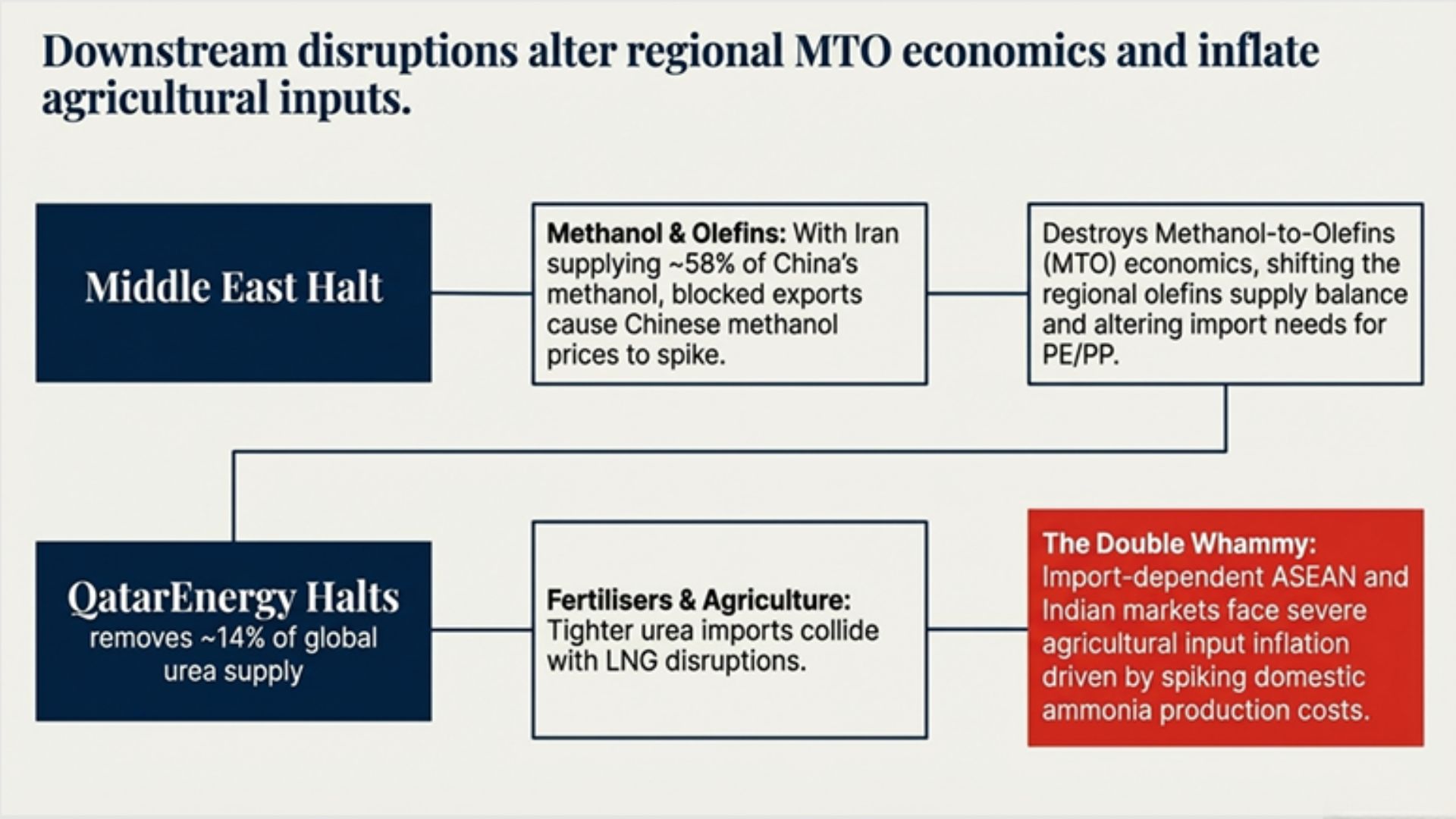

- China: the exposure is both feedstock and product linked. ICIS highlights the methanol channel: ~70% of China’s methanol imports originate from the Middle East, and Iran accounted for ~58% of China’s methanol imports in 2025 (corrected ICIS figure).

- Thailand and Vietnam: the policy response illustrates domestic energy-security stress that can cascade into petrochem allocation. ICIS reports Thailand’s fuel export ban aimed at maintaining strategic reserves, and Reuters reports Binh Son Refining and Petrochemical asked the government to prioritize domestic crude supply and limit exports through at least end-Q3 to ensure national security.

- India: while your question centers on SEA/APAC, India remains a major marginal buyer and price-setter for multiple chains. Reuters highlights India’s vulnerability to supply shocks given reserve constraints, while brokerage commentary expects tightening availability for propylene, methanol, styrene, and polymers in a prolonged disruption scenario.

Why “feedstock substitution” only partially solves it

A common mitigation assumption is: “crackers can switch feedstock.” ICIS provides a reality-check:

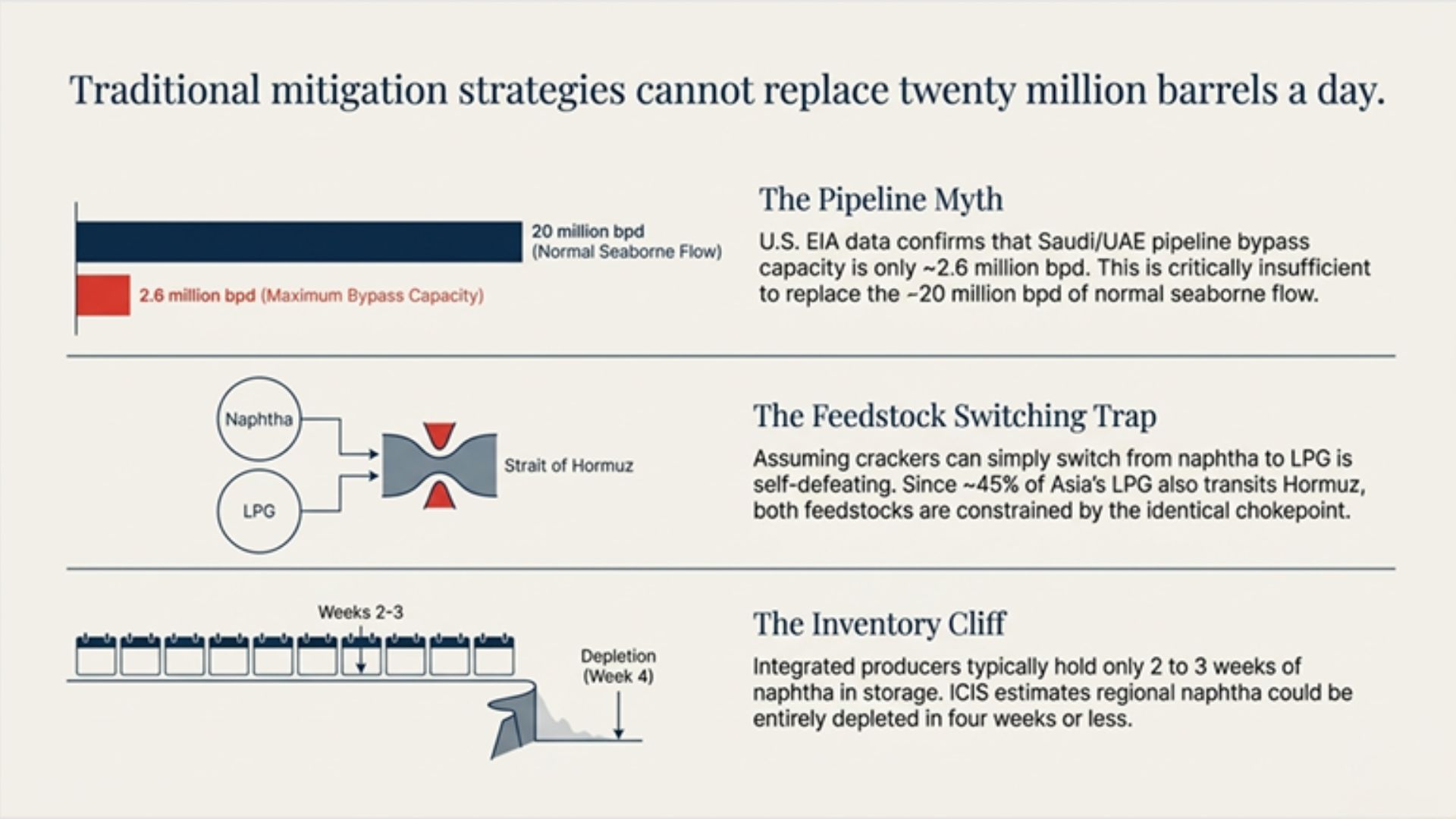

- More than 60% of Asia’s seaborne naphtha demand is Middle East-covered, and ~45% of Asia’s LPG imports move via Hormuz—meaning substitution from naphtha to LPG can become self-defeating when both are constrained by the same chokepoint.

- Integrated producers often have 2–3 weeks of naphtha in storage, which buys time but also creates a visible “cliff” if the disruption lasts beyond typical inventory cover.

Expected market impacts by chemical chain

A useful way to think about price formation in SEA/APAC from here is: (a) feedstock scarcity + (b) freight/insurance inflation + (c) pre-existing overcapacity/weak demand. The weights shift by product chain.

Olefins and polyolefins

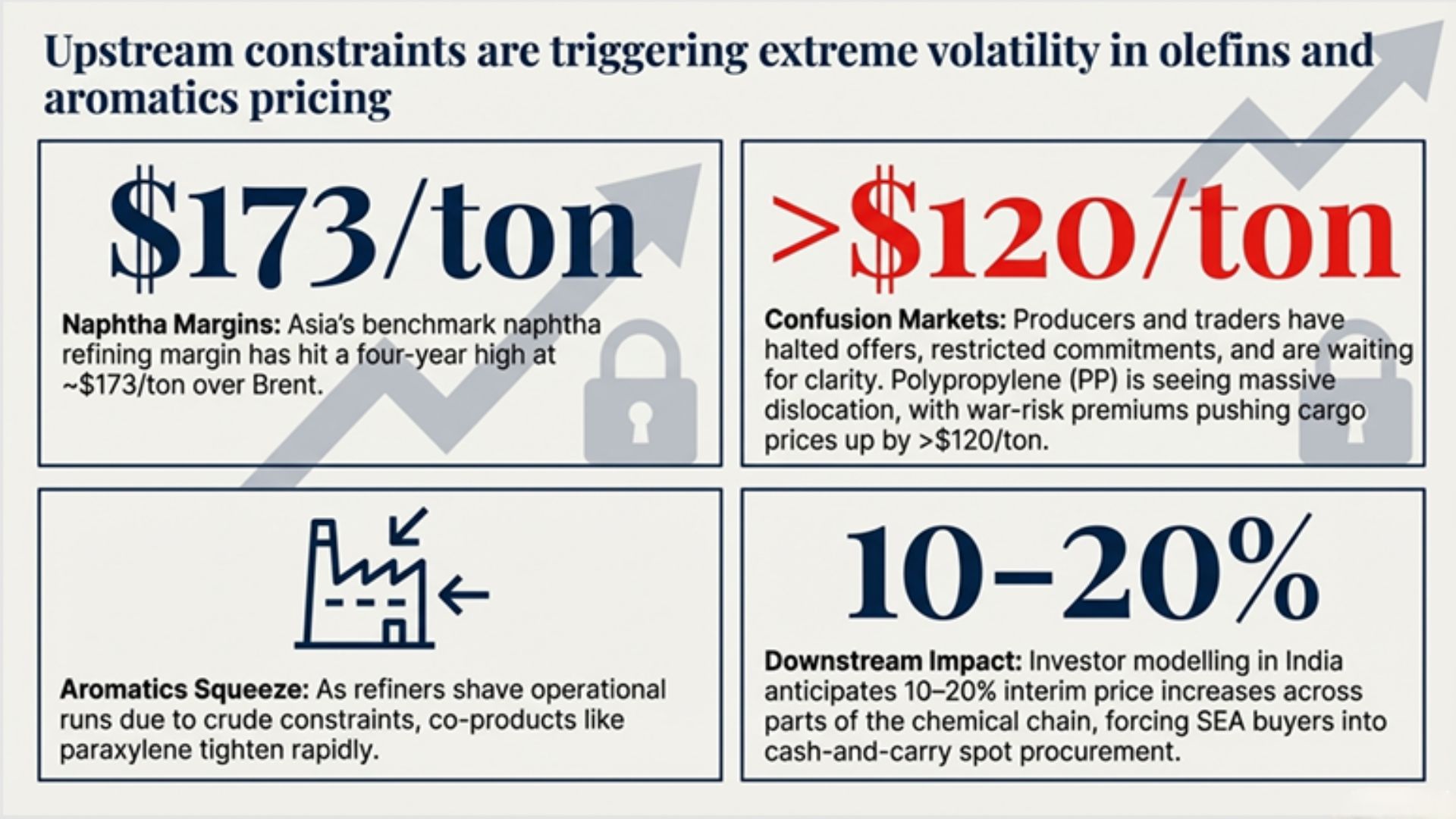

- Naphtha disruption is no longer abstract: Reuters reports Asia sources ~4 million metric tons of Middle East naphtha monthly, and the supply squeeze pushed the benchmark naphtha refining margin to about $173/ton over Brent (a four-year high).

- ICIS reports a behavioral shift typical of “confusion markets”: producers and traders halting offers, waiting for clarity, and restricting commitments.

The polypropylene market illustrates how fast delivered prices can gap up: ICIS cites route suspensions and war-risk premiums (examples cited at $120/ton and more on cargoes into/out of the Middle East) and sharp week-to-week changes in CFR SEA indications for PP cargoes.

Implications for SEA buyers (packaging, consumer goods, industrial converters): expect shorter order horizons, supplier allocation, and greater emphasis on cash-and-carry spot procurement—especially where converters cannot fully pass through resin cost increases within their own customer contracts.

Aromatics and refinery–petchem integration

Aromatics are indirectly impacted even when the direct aromatics cargo route is not blocked, because they are often co-produced alongside the broader refinery–naphtha system.

- ICIS notes that if refiners shave runs due to crude constraints, downstream products like paraxylene can be curtailed, tightening supply even in chains that were previously long.

- Reuters describes Asia refiners cutting operations and seeking alternatives, while also reporting surges in regional refining margins; these margin shifts can change optimal refinery output slates, which then affects naphtha availability for petrochem buyers.

Methanol and MTO-linked exposure

Methanol is one of the most “non-linear” shock channels because it sits at the intersection of:

- Iran’s export capacity,

- shipping access, and

China’s MTO economics

ICIS reports that Iran accounted for ~58% of China’s methanol imports in 2025 and that methanol prices/futures in China rose as Middle East export disruptions were priced in.

For SEA/APAC, the key point is not only methanol price; it’s that methanol-to-olefins economics can alter regional olefins supply balance, changing import needs for PE/PP and shifting arbitrage flows. This is a second-order transmission mechanism, supported by ICIS’s description of reshaped resin market behavior (halted offers, stopped negotiations) once methanol and naphtha uncertainty rises.

Fertilizers, ammonia, and urea-linked chemicals

Fertilizers matter for SEA/APAC chemical markets because they affect:

- agricultural input inflation (agrochem demand timing), and

upstream ammonia pricing (chemical feedstock and energy linkage).

QatarEnergy stated it would halt polymer, urea, and methanol production after attacks on facilities; entity[“organization”, “Chemical & Engineering News”, “chemistry news magazine”] reports Qatar has annual capacity of 5.6 million metric tons of urea (~14% of global supply) and supplies ~20% of the world’s LNG (per Kpler).

Brokerage commentary in India explicitly frames a “double whammy” risk: tighter ammonia/urea imports plus LNG disruption impacting ammonia production costs. While this is India-focused, the same logic extends to import-dependent ASEAN fertilizer markets, particularly if LNG tightness becomes prolonged.

Trade-flow and competitive dynamics

The competitive “winners and losers” here depend on the duration of disruption and the balance between supply tightening and demand destruction.

Limited bypass capacity means some tightening is hard to avoid

U.S. Energy Information Administration estimates that only about 2.6 million b/d of Saudi/UAE pipeline capacity could be available (in a disruption scenario) to bypass Hormuz—small versus the ~20 million b/d of oil flows normally transiting the strait in 2024.

So even with diversion to non-Hormuz ports and pipeline use, expect partial mitigation, not full replacement—especially in a scenario where shipping risk persists long enough that storage at origin begins to fill (a theme also present in S&P’s reporting about floating storage dynamics and producers facing shut-ins).

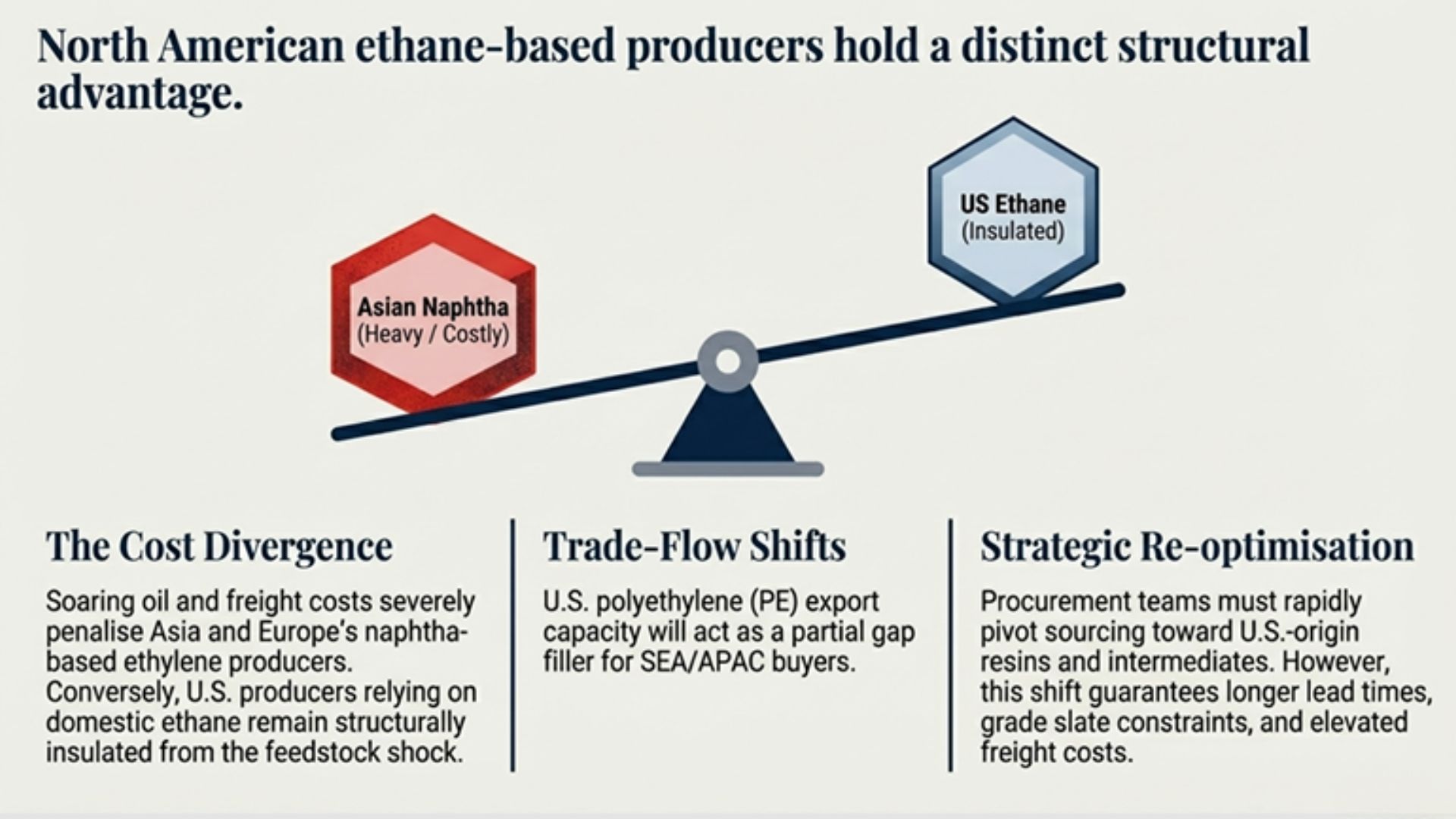

North America’s ethane advantage can translate into APAC market share

Multiple sources converge on the relative advantage of ethane-based producers during crude-linked volatility:

- entity [“organization”,”Chemical & Engineering News”,”chemistry news magazine”] explicitly notes that higher oil prices raise costs for Asia/Europe naphtha-based ethylene, while U.S. producers using ethane are relatively insulated.

The IOM3 summary (republishing ICIS-referenced analysis) points to U.S. PE export capacity as a partial “gap filler,” but not enough to fully replace Middle East exports in an extreme outcome.

For SEA/APAC buyers, that implies a likely re-optimization of sourcing: more U.S.-origin resin and intermediates where logistics and trade policy allow, but at higher freight/longer lead times—and with possible grade slate constraints.

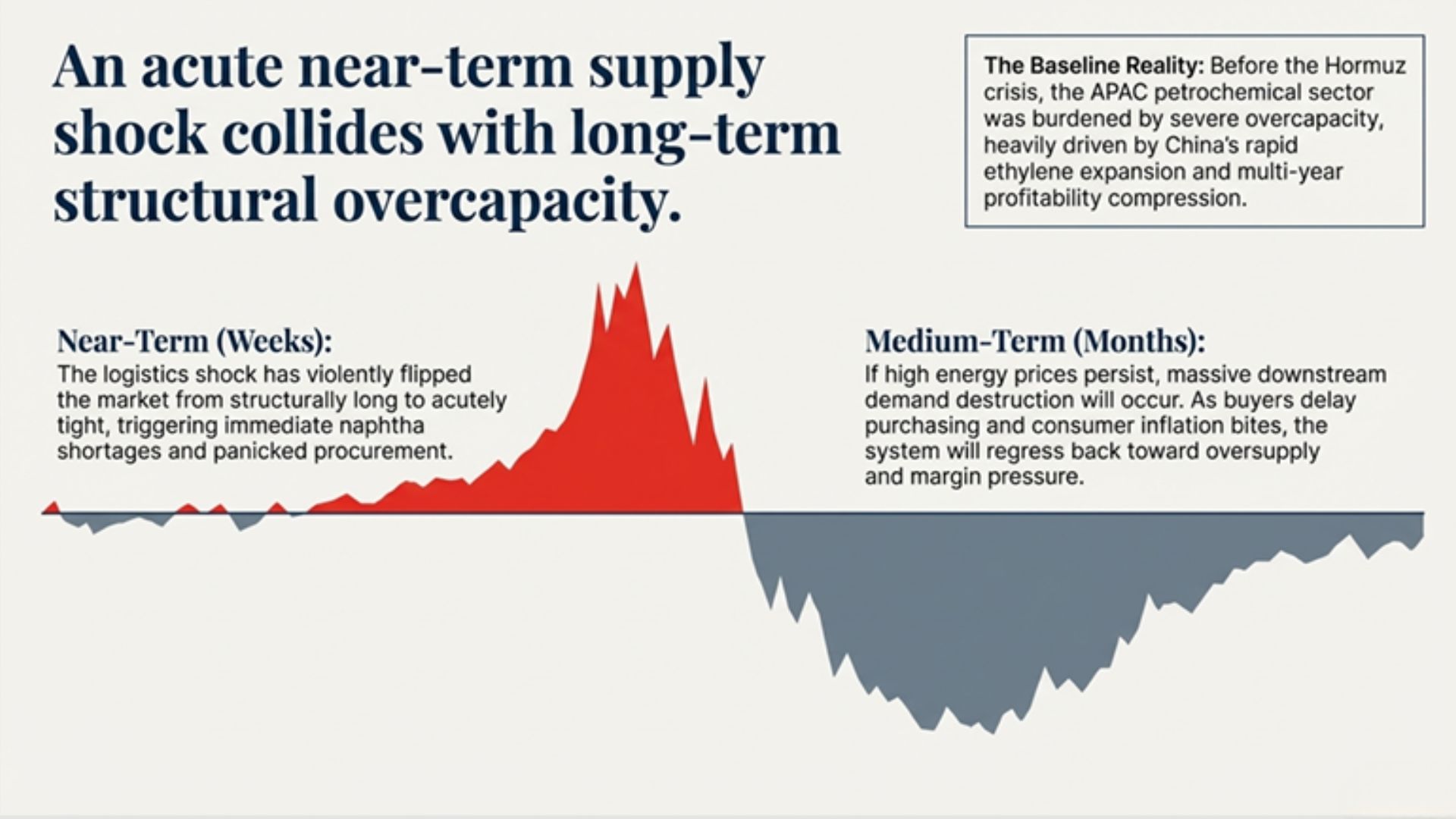

China’s overcapacity backdrop changes how persistent the shock feels

Before Hormuz, APAC petrochem was already grappling with oversupply and margin pressure:

- C&EN reporting on the region highlights China’s rapid ethylene capacity growth and the resulting export pressure on other Asian countries, alongside Japanese consolidation and sustained sub-80% operating rates in parts of Japan’s cracker system.

C&EN also reports multi-year price index declines and profitability compression in China’s chemical sector, linked to overcapacity and weak demand.

This matters because it creates two competing regimes:

- Near-term (weeks): a supply shock can flip markets from “long” to “tight” quickly (ICIS explicitly describes a shift from structural oversupply to acute naphtha shortage).

Medium-term (months): if high energy prices persist, downstream demand can weaken (buyers delay purchasing, consumer price inflation rises), pushing the system back toward oversupply—especially in commoditized chains exposed to China’s export capacity.

Price discovery and contracting friction increase

Reuters reports that S&P Global Platts suspended bids/offers for some Middle East assessments and related refined products/LNG offers due to shipping disruption and safety concerns, which can reduce liquidity and complicate hedging/contract benchmarks.

In practical procurement terms, SEA/APAC chemical companies should expect:

- more “subject to safe transit” clauses,

- wider bid-ask spreads and shorter quote validity windows, and

- potential renegotiation of delivery terms (FOB → CFR shifts, or alternative loading ports).

Talent and hiring outlook in SEA and wider APAC

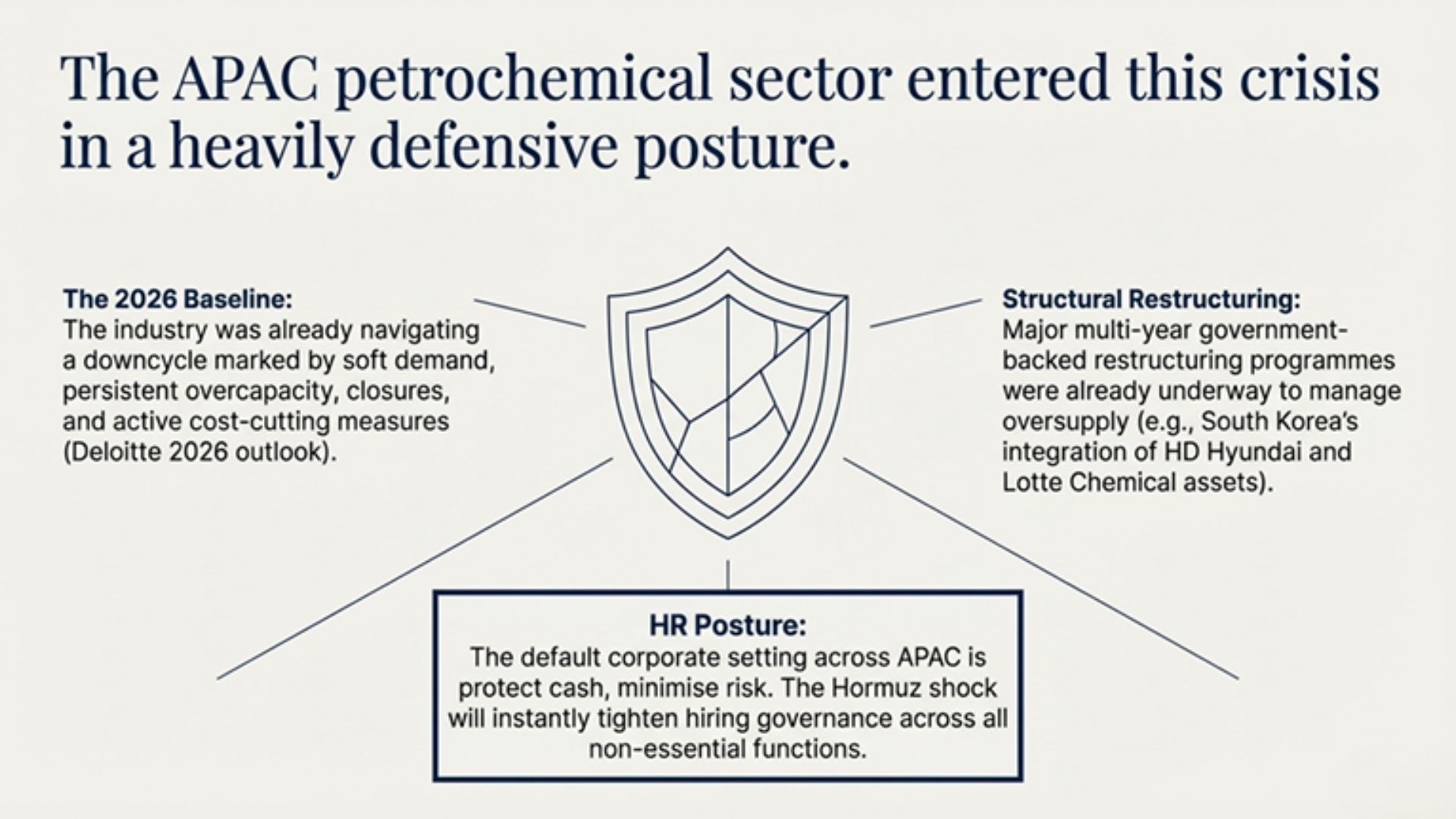

Baseline: APAC petrochemicals were already in a defensive posture

Even before the Hormuz shock, leading indicators pointed to a cautious stance across commodity chemicals:

- Deloitte’s 2026 outlook emphasizes a downcycle characterized by soft demand, persistent overcapacity, cost cutting, closures/divestments, and capex pullback (including layoffs and delayed maintenance as part of SG&A reduction).

In South Korea, oversupply-driven restructuring is now formal policy: Ministry of Trade, Industry and Resources outlines a multi-year restructuring project integrating assets of HD Hyundai Oilbank, HD Hyundai Chemical, and Lotte Chemical, with explicit acknowledgement of measures to address employment challenges in affected regions.

This baseline means many companies entered March 2026 with a “protect cash, minimize risk” mindset, so a logistics shock tends to tighten hiring governance quickly.

Near-term hiring likely to rise in “continuity-critical” roles

Across SEA/APAC, the positions most likely to stay active (or be fast-tracked) are the ones that manage the shock directly:

- Feedstock procurement and alternative sourcing (naphtha, LPG, condensate, methanol) as buyers respond to the time-compressed need to pivot supply (Reuters highlights “within two weeks” decisions for Korean buyers).

- Trading, scheduling, chartering, and claims (force majeure documentation, contract renegotiations, demurrage, insurance coordination) because war-risk costs and transit uncertainty are rising (Reuters and S&P describe surging war-risk and elevated marine insurance costs).

- Planning/IBP and demand management (allocation, substitution, rationing) as suppliers halt offers and downstream converters rush to secure cargoes before further increases (observed in ICIS PP market commentary).

HSE/process safety/reliability leadership, particularly for plants operating at minimum rates or undertaking unplanned slowdowns (because risk increases during abnormal operations), consistent with the operational reality described in force majeure notices and minimum-capacity operations.

Roles tied to day-to-day running and supply-chain continuity are less likely to be paused; if anything, they can become “must-fill” due to immediate risk exposure and cost of downtime.

Roles most exposed to pause/re-scoping

Hiring risk tends to rise for roles that depend on stable forward visibility:

- Discretionary growth capex and some project development roles, because companies often delay big investment decisions during periods of geopolitical volatility and uncertain margins (explicitly flagged in Deloitte’s outlook).

- Commodity expansion roles at naphtha-based sites already under margin pressure (APAC’s overcapacity context), particularly if higher feedstock costs persist and downstream demand weakens.

- Some commercial roles tied to long-horizon volume growth in commoditized chains, because contracting can shift to allocations and shorter-term deals when suppliers declare force majeure.

Where hiring could surprise on the upside

Certain segments can see counter-cyclical hiring under volatility:

- Specialty chemical companies with stronger pass-through pricing or inventory advantage (broker commentary highlights inventory-driven benefits in some chains when prices rise).

- Regional refiners and integrated producers capturing high refining margins (Reuters reports sharply higher refining margins and multi-year/record highs in products like jet fuel and gasoil cracks, which can support near-term profitability and maintenance/operations staffing).

- Compliance, trade controls, and sanctions-risk roles if alternative sourcing shifts toward sanctioned/gray-market barrels or non-standard trading routes (Reuters notes discussion of alternative supply including Russian naphtha in a “dire scenario,” which typically increases compliance burden).

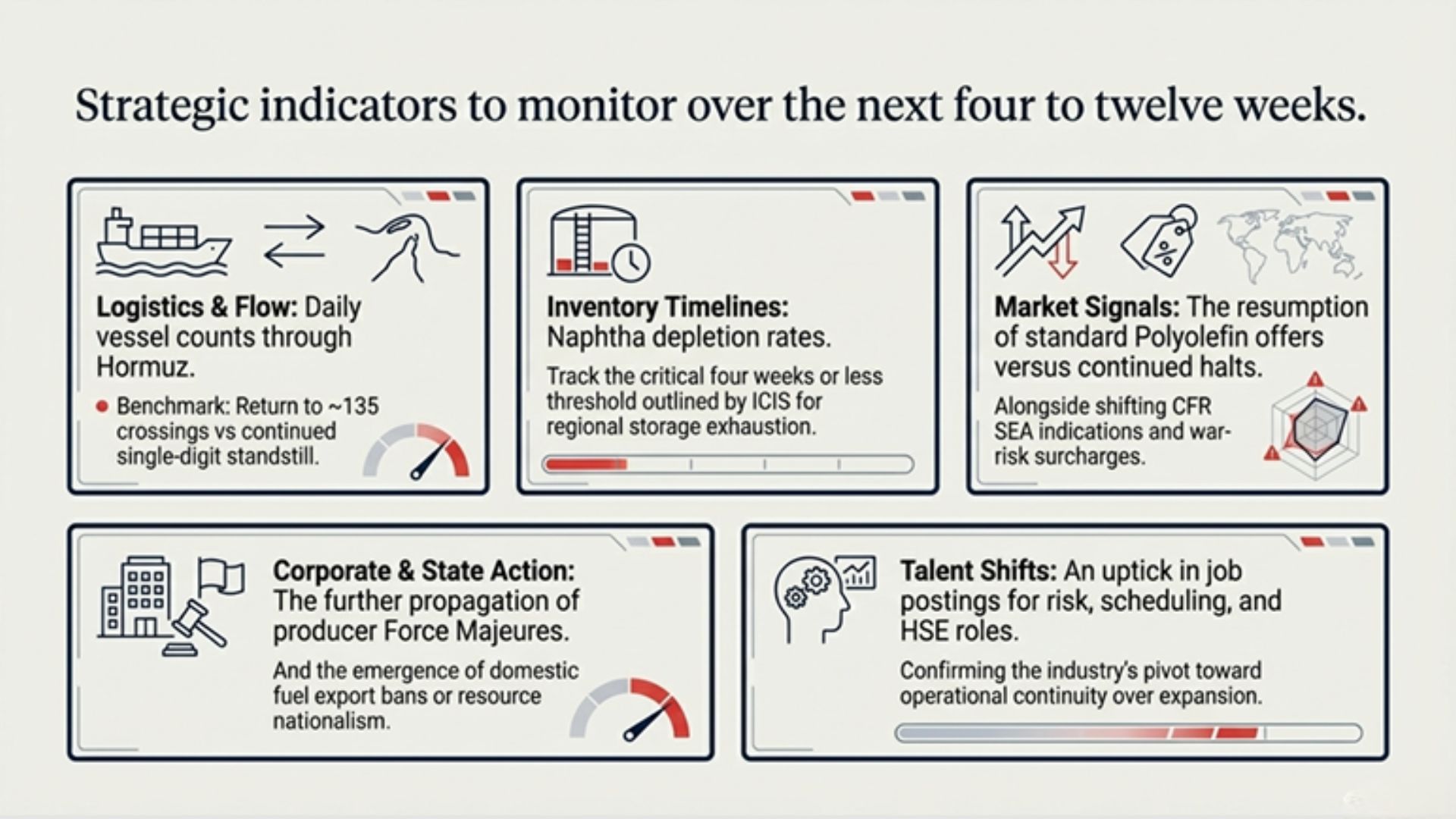

What to monitor over the next four to twelve weeks

Because this crisis is moving quickly, SEA/APAC chemical-market decisions benefit from tracking a small set of “leading indicators” that connect directly to production and hiring behavior.

- Transit normalization vs persistent standstill: daily vessel counts through Hormuz (S&P’s “135 to 7 vessels” framing is a practical benchmark for “normal vs disrupted”).

- Naphtha and LPG replacement feasibility: watch for confirmation of prolonged Middle East supply constraint and for signs that alternative cargoes (U.S./South Asia) are arriving in volumes sufficient to prevent regional inventory depletion (ICIS’s “four weeks or less” depletion framing is the key time horizon).

- Force majeure propagation: whether additional SEA producers follow PCS/Chandra Asri patterns, and whether force majeure lifts or extends (PCS explicitly says duration and full extent are uncertain).

- Polyolefin offer behavior and converter substitution: resumption of offers vs continued “halt” behavior in SEA PP/PE, plus movement in CFR SEA indications and war-risk surcharge levels (ICIS provides concrete, early price-behavior examples).

- Government interventions: fuel export bans and domestic allocation policies (Thailand, China, Vietnam examples) can signal broader “resource nationalism” behavior that tighter chemical-market availability.

- Hiring signals: increases in postings/mandates for procurement, scheduling, risk, and HSE roles versus pauses in capex/project hiring—consistent with how chemical firms behave in a downcycle with heightened uncertainty.

- Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint – U.S. Energy Information Administration (EIA) – https://www.eia.gov/todayinenergy/detail.php?id=65504

- FACTBOX: Hormuz oil flows still at a standstill despite US insurance pledge | S&P Global – https://www.spglobal.com/energy/en/news-research/latest-news/refined-products/030426-factbox-hormuz-oil-flows-still-at-a-standstill-despite-us-insurance-pledge

- Corrected: INSIGHT: Mideast conflict threatens Asia petrochemical production | ICIS – https://www.icis.com/explore/resources/news/2026/03/04/11185153/insight-mideast-conflict-threatens-asia-petrochemical-production/

- PCS Pte. Ltd. Issues Formal Notice of Force Majeure | PCS Pte. Ltd. – https://www.pcs.com.sg/news-post/pcs-pte-ltd-issues-formal-notice-of-force-majeure

- Latest News | PCS Pte. Ltd. – https://www.pcs.com.sg/news/latest-news/

- Internal Error

- Industry < TOPICS – Ministry of Trade, industry and Energy – https://english.motir.go.kr/eng/12/topics/

- https://cen.acs.org/business/petrochemicals/Iran-war-hits-chemical-sector/104/web/2026/03 – https://cen.acs.org/business/petrochemicals/Iran-war-hits-chemical-sector/104/web/2026/03

- S Korea Feb petrochemical exports fall 15.4% amid global oversupply | ICIS – https://www.icis.com/explore/resources/news/2026/03/02/11184106/s-korea-feb-petrochemical-exports-fall-15-4-amid-global-oversupply

- Asia PP market faces severe supply disruptions as a result of Middle East conflict | ICIS – https://www.icis.com/explore/resources/news/2026/03/03/11184799/asia-pp-market-faces-severe-supply-disruptions-as-a-result-of-middle-east-conflict

- Asia refineries cut runs on Middle East oil disruption –

- https://www.reuters.com/business/energy/asia-refineries-cut-runs-middle-east-oil-disruption-2026-03-05/

- MOTIR Approves First Petrochemical Restructuring Project, Unveils Support Package of Over KRW 2.1 Trillion < Press Releases < PRESS CENTER < Ministry of Trade, Industry and Resources –

- https://english.motir.go.kr/eng/article/EATCLdfa319ada/2512/view

- https://cen.acs.org/business/petrochemicals/Deluge-petrochemicals-China-swamps-Asian/104/web/2026/01 – https://cen.acs.org/business/petrochemicals/Deluge-petrochemicals-China-swamps-Asian/104/web/2026/01

- https://cen.acs.org/business/Chinas-chemical-makers-face-headwinds/104/web/2026/01

- https://cen.acs.org/business/Chinas-chemical-makers-face-headwinds/104/web/2026/01

- Iran conflict disrupts Middle East oil, fuel, LNG assessments from reporting agency Platts – https://www.reuters.com/world/middle-east/platts-reviewing-mideast-crude-pricing-mechanism-amid-us-israel-attacks-iran-2026-03-02/

- Asia refining margins rocket to highest in nearly 4 years on Hormuz supply disruption – https://www.reuters.com/business/energy/asia-refining-margins-rocket-highest-nearly-4-years-hormuz-supply-disruption-2026-03-05/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}